Unicorns and Funding - Outlook for 2023

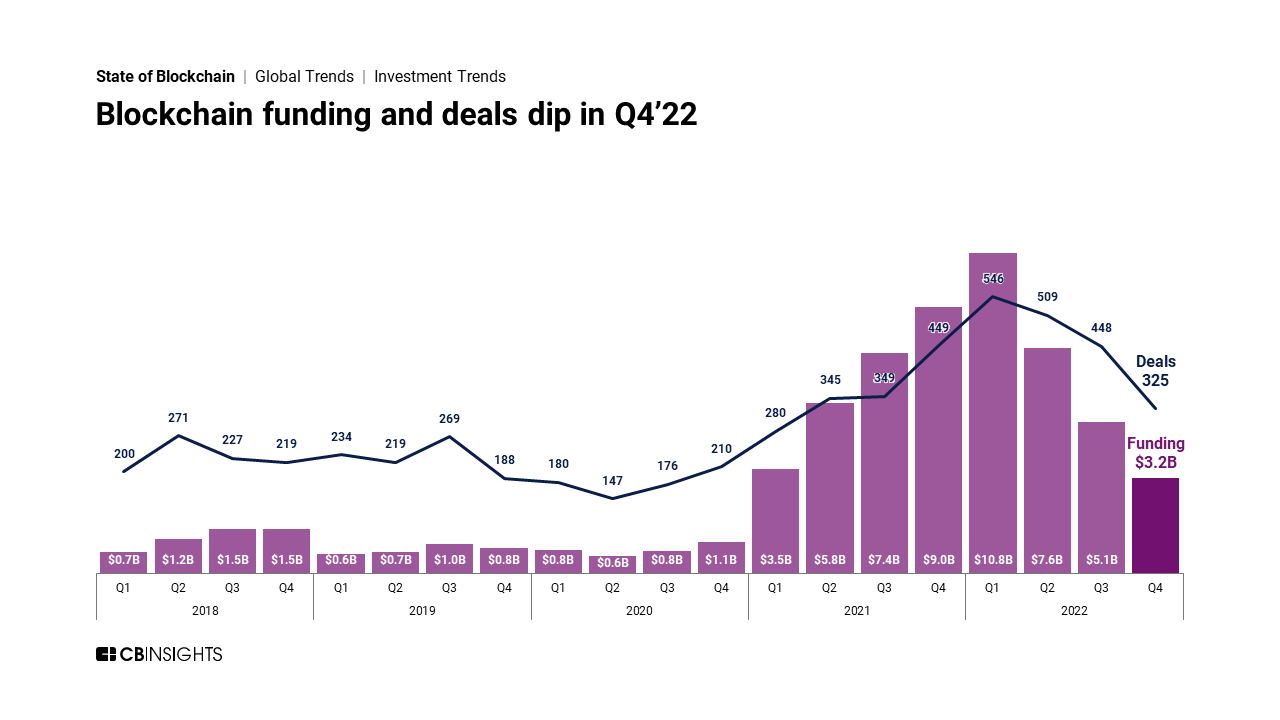

Let me start with my favorite topic - Global venture funding to blockchain and crypto companies reached a new record of $26.8B in 2022, largely propped up by a strong first half. But as the year progressed, the crypto winter coupled with macroeconomic pressures caused 3 straight quarters of declines in funding and deals.

By the end of Q4’22, quarterly blockchain funding had fallen 70% from the start of the year to hit its lowest level since 2020. After 2 consecutive quarters of decline, this down quarter didn’t really come as a surprise after the November’s FTX’s bankruptcy.

2022 highlights across the blockchain ecosystem include:

Blockchain venture funding grew 4% year-over-year (YoY) to reach $26.8B in 2022 thanks to a strong H1.

The average deal size to blockchain startups fell 24% YoY to $16.2M in 2022, driven by a sharp drop in $100M+ mega-rounds throughout the year.

The blockchain unicorn count stalled out at 79 at the end of 2022, with just 2 new unicorns in Q4’22.

Web3 startups accounted for 56% of blockchain venture funding in 2022, up from 39% last year.

Blockchain infrastructure & development had a record year for funding ($7.8B) and deals (235) in 2022, signaling investor confidence in blockchain’s future irrespective of cryptocurrency volatility.

Venture funding to crypto exchanges & wallets fell 48% YoY in 2022, revealing a clear shift in investor sentiment away from centralized exchanges.

Overall, for a relatively young industry growing in “dog years”, we are doing great on the Unicorns front!

For the ful overview check CBI State of Blockchain 2022 Report.

As the blockchain ecosystem is still alien to many, I love that the summary is brief, straight to the point and not that different from the trends one can see in traditional funding. However, CBI had to name it “Blockchain poops the bed”.

The number of global unicorns (private companies valued at $1B+) soared in 2021 and into 2022, until macro trends like inflation, rising interest rates, and geopolitical crises shocked the public markets, putting downward pressure on some of the world’s most highly valued companies. Q4’22 became the lowest quarterly figure in over 5 years.

What’s driving the downward trend and how this affects global regions and sectors, valuations and funding?

2021’s unicorn stampede: The exuberant funding environment in 2021 — fueled by pandemic tailwinds like near-zero interest rates and the rapid adoption of digital technologies — drove unicorn births to record highs. During that time, crossover investors like Tiger Global Management and Coatue Management ratcheted up their private-market dealmaking, pouring massive amounts of capital into funding rounds that sent valuations skyrocketing. In 2022, however, the meteoric growth has not been able to sustain itself.

Unstable macro conditions: The upward momentum continued into early 2022, with the unicorn list reaching 1,000 for the first time in February. However, macro trends like inflation, rising interest rates, and geopolitical crises — such as the war in Ukraine — arose to shock the public markets.

Some previously high-flying tech stocks, such as pandemic darlings like Robinhood and Zoom, as well as big tech giants, plunged, and many late-stage startups delayed or canceled plans to go public.

The venture market tightens: This year, venture funding has shrunk with each passing quarter, with some crossover investors pulling back significantly after experiencing massive losses in their public funds.

Mirroring their public-market peers, several high-profile, late-stage startups have already seen their valuations slashed. Some investors have also marked down the value of their private-company portfolios.

Exits cool off: The decline in unicorn births cannot simply be attributed to more companies exiting before they can raise unicorn-minting rounds. The uncertainty of public market performance is keeping many late-stage companies from seeking an exit via IPO or SPAC, especially in the US. In Q2’22, M&A deals fell to their lowest level since Q4’20.

Volatility in the public markets — fueled by an unstable macro environment — has put downward pressure on the most valuable private companies, forcing valuations to contract and driving investors away from large, late-stage rounds.

The US and Asia have been most affected by the unicorn slowdown. Europe, on the other hand, watched its share of total unicorns increase quarter-over-quarter (QoQ) in Q2’22.

Fintech has been hit hard, seeing a larger QoQ decline in new unicorns than any other sector. Meanwhile, digital health has remained resilient.

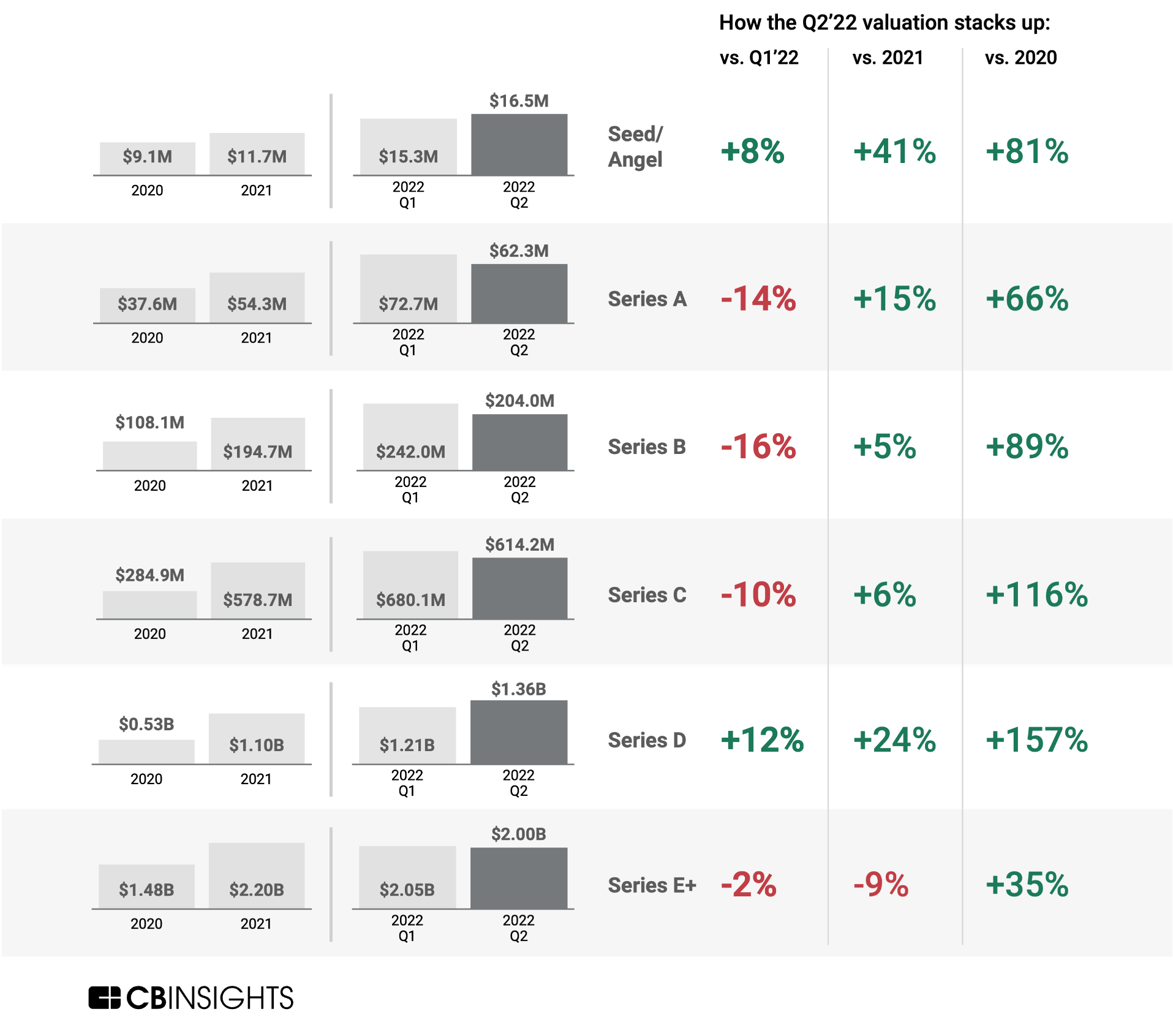

Median valuations have fallen modestly across most investment stages, but there’s plenty of room for them to fall further.

The power balance is shifting from founders to investors, who now have more leverage to invest at cheaper prices or structure deals for more downside protection.

Today’s abundance of unicorns is a vestige of 2021’s bullish venture ecosystem. Valuations fell modestly across most investment stages in Q2’22, but there’s room for them to fall further.

In Q2’22, only Series E+ rounds saw their median valuation fall below the full-year 2021 level. These have been the rounds most directly impacted by public market volatility.

Companies that raised large funding rounds in 2021 may be able to hold out for some time without needing to seek out more capital. However, companies burning through their cash may be forced to raise funding at a potentially significant discount. As an example, Sweden-based buy now, pay later (BNPL) unicorn Klarna’s valuation skyrocketed during the pandemic to reach $45.6B in June 2021. After being driven up by online spending habits, its valuation came crashing down in July 2022. The company raised $800M in funding at a $6.7B valuation — an 85% drop.

Investors will seek out startups that are profitable and can use capital efficiently (for instance, not burning it at high rates to maintain growth). Unicorns will likely avoid raising new funding if they can survive on their current cash not to lower their valuations. Otherwise, they may seek alternative deal terms — such as raising venture debt instead of equity or structuring deals to give investors a potentially higher payout — that limit the damage to their valuation or avoid a disclosed valuation altogether.

In this environment, companies will need to demonstrate they can balance sustainable growth with profitability to have a chance at reaching — or holding onto — a coveted $1B+ valuation.

Impact on Fundraising

A tighter funding environment — where investors are not competing as intensely for access to deals — means there will be fewer deals at the unicorn level, making it harder for any given company to achieve a valuation north of $1B. investors have retreated from backing the late-stage companies that are most exposed to public market volatility. Tiger Global Management, has already shifted a vast portion of its private-market investing toward early-stage deals. It also announced that it would slow overall dealmaking through the end of the year.

Fifty-one private companies (4.2% of total unicorns) fall within the next bracket — the “decacorns,” worth between $10B and $100B. ByteDance was the only private company considered to be a “hectocorn” (worth $100B+) — until October 2021, when SpaceX eclipsed that mark. Shein has since joined the ranks of the hectocorns as well.

Fintech is the most highly represented category - roughly 1 in 5 unicorns (20.9%). It is followed by internet software & services (18.9%), e-commerce & direct-to-consumer (9.0%), and health (8.0%).

Geographical trends are the most curious! Globally, a total of 47 countries and regions are represented in the unicorn club. However:

53.9% - the leading unicorn share belongs to the US

14.3% belong to China

5.7% - India

the UK has only 4.2% of unicorns

While the fintech sector accounted for 1 in 4 global unicorn club members in Q2’22, it saw its share of new unicorn births fall more than any other sector we analyzed. Its 20 new unicorns represented a decline of 44% QoQ and 58% YoY. The top fintech unicorn births in Q2’22 were KuCoin ($10B), Coda Payments ($2.5B), and Newfront Insurance ($2.2B).

The digital health sector held steady QoQ with 8 new unicorns. That number is down just 27% YoY, the least among sectors analyzed. The quarter’s top new unicorns were my favourite Oura ($2.6B), Clarify Health ($1.4B) and Biofourmis ($1.3B).

For the full list of Unicorns see the below data as of 1/6/2023.

{kind=link}

{kind=link}

Categories are not mutually exclusive and companies are sorted by primary use case. Data is as of 1/6/2023.